pmdarima-python-3.13.1

Update pmdarima compatible with Python 3.13.1

Science Score: 44.0%

This score indicates how likely this project is to be science-related based on various indicators:

-

✓CITATION.cff file

Found CITATION.cff file -

✓codemeta.json file

Found codemeta.json file -

✓.zenodo.json file

Found .zenodo.json file -

○DOI references

-

○Academic publication links

-

○Academic email domains

-

○Institutional organization owner

-

○JOSS paper metadata

-

○Scientific vocabulary similarity

Low similarity (15.6%) to scientific vocabulary

Repository

Update pmdarima compatible with Python 3.13.1

Basic Info

- Host: GitHub

- Owner: JonasVeronez

- License: mit

- Language: Python

- Default Branch: master

- Size: 1.37 MB

Statistics

- Stars: 1

- Watchers: 0

- Forks: 0

- Open Issues: 0

- Releases: 0

Metadata Files

README.md

pmdarima

![]()

![]()

![]()

![]()

Pmdarima (originally pyramid-arima, for the anagram of 'py' + 'arima') is a statistical

library designed to fill the void in Python's time series analysis capabilities. This includes:

- The equivalent of R's

auto.arimafunctionality - A collection of statistical tests of stationarity and seasonality

- Time series utilities, such as differencing and inverse differencing

- Numerous endogenous and exogenous transformers and featurizers, including Box-Cox and Fourier transformations

- Seasonal time series decompositions

- Cross-validation utilities

- A rich collection of built-in time series datasets for prototyping and examples

- Scikit-learn-esque pipelines to consolidate your estimators and promote productionization

Pmdarima wraps statsmodels under the hood, but is designed with an interface that's familiar to users coming from a scikit-learn background.

Installation

pip

Pmdarima has binary and source distributions for Windows, Mac and Linux (manylinux) on pypi

under the package name pmdarima and can be downloaded via pip:

bash

pip install pmdarima

conda

Pmdarima also has Mac and Linux builds available via conda and can be installed like so:

bash

conda config --add channels conda-forge

conda config --set channel_priority strict

conda install pmdarima

Note: We do not maintain our own Conda binaries, they are maintained at https://github.com/conda-forge/pmdarima-feedstock. See that repo for further documentation on working with Pmdarima on Conda.

Quickstart Examples

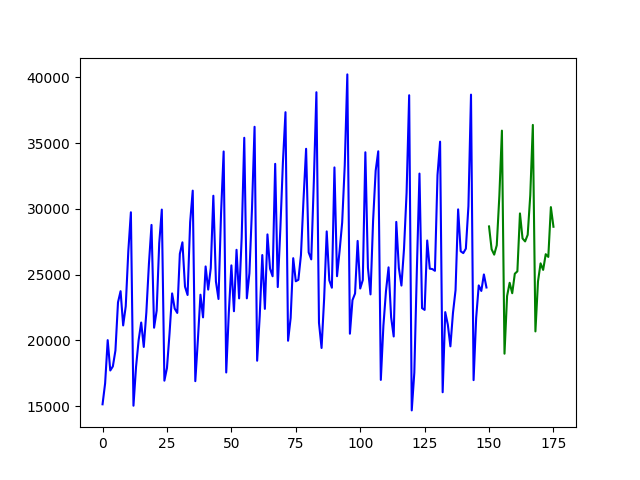

Fitting a simple auto-ARIMA on the wineind dataset:

```python import pmdarima as pm from pmdarima.modelselection import traintest_split import numpy as np import matplotlib.pyplot as plt

Load/split your data

y = pm.datasets.loadwineind() train, test = traintestsplit(y, trainsize=150)

Fit your model

model = pm.auto_arima(train, seasonal=True, m=12)

make your forecasts

forecasts = model.predict(test.shape[0]) # predict N steps into the future

Visualize the forecasts (blue=train, green=forecasts)

x = np.arange(y.shape[0]) plt.plot(x[:150], train, c='blue') plt.plot(x[150:], forecasts, c='green') plt.show() ```

Fitting a more complex pipeline on the sunspots dataset,

serializing it, and then loading it from disk to make predictions:

```python import pmdarima as pm from pmdarima.modelselection import traintest_split from pmdarima.pipeline import Pipeline from pmdarima.preprocessing import BoxCoxEndogTransformer import pickle

Load/split your data

y = pm.datasets.loadsunspots() train, test = traintestsplit(y, trainsize=2700)

Define and fit your pipeline

pipeline = Pipeline([ ('boxcox', BoxCoxEndogTransformer(lmbda2=1e-6)), # lmbda2 avoids negative values ('arima', pm.AutoARIMA(seasonal=True, m=12, suppress_warnings=True, trace=True)) ])

pipeline.fit(train)

Serialize your model just like you would in scikit:

with open('model.pkl', 'wb') as pkl: pickle.dump(pipeline, pkl)

Load it and make predictions seamlessly:

with open('model.pkl', 'rb') as pkl: mod = pickle.load(pkl) print(mod.predict(15))

[25.20580375 25.05573898 24.4263037 23.56766793 22.67463049 21.82231043

21.04061069 20.33693017 19.70906027 19.1509862 18.6555793 18.21577243

17.8250318 17.47750614 17.16803394]

```

Availability

pmdarima is available on PyPi in pre-built Wheel files for Python 3.9+ for the following platforms:

- Mac (64-bit)

- Linux (64-bit manylinux)

- Windows (64-bit)

- 32-bit wheels are available for pmdarima versions below 2.0.0 and Python versions below 3.10

If a wheel doesn't exist for your platform, you can still pip install and it

will build from the source distribution tarball, however you'll need cython>=0.29

and gcc (Mac/Linux) or MinGW (Windows) in order to build the package from source.

Note that legacy versions (<1.0.0) are available under the name

"pyramid-arima" and can be pip installed via:

```bash

Legacy warning:

$ pip install pyramid-arima

python -c 'import pyramid;'

```

However, this is not recommended.

Documentation

All of your questions and more (including examples and guides) can be answered by

the pmdarima documentation. If not, always

feel free to file an issue.

Owner

- Login: JonasVeronez

- Kind: user

- Repositories: 2

- Profile: https://github.com/JonasVeronez

Citation (CITATION.cff)

cff-version: 1.2.0 message: "If you would like to include pmdarima in your published work, please cite it as follows" authors: - family-names: "Smith" given-names: "Taylor G." keywords: - python - "machine learning" - "time series" - econometrics - forecasting - arima - "forecasting models" - sarimax title: "pmdarima" version: 2.0.4 date-released: 2023-10-23 license: MIT repository-artifact: https://pypi.org/project/pmdarima repository-code: https://github.com/alkaline-ml/pmdarima

GitHub Events

Total

- Watch event: 2

- Public event: 2

- Push event: 3

- Create event: 2

Last Year

- Watch event: 2

- Public event: 2

- Push event: 3

- Create event: 2